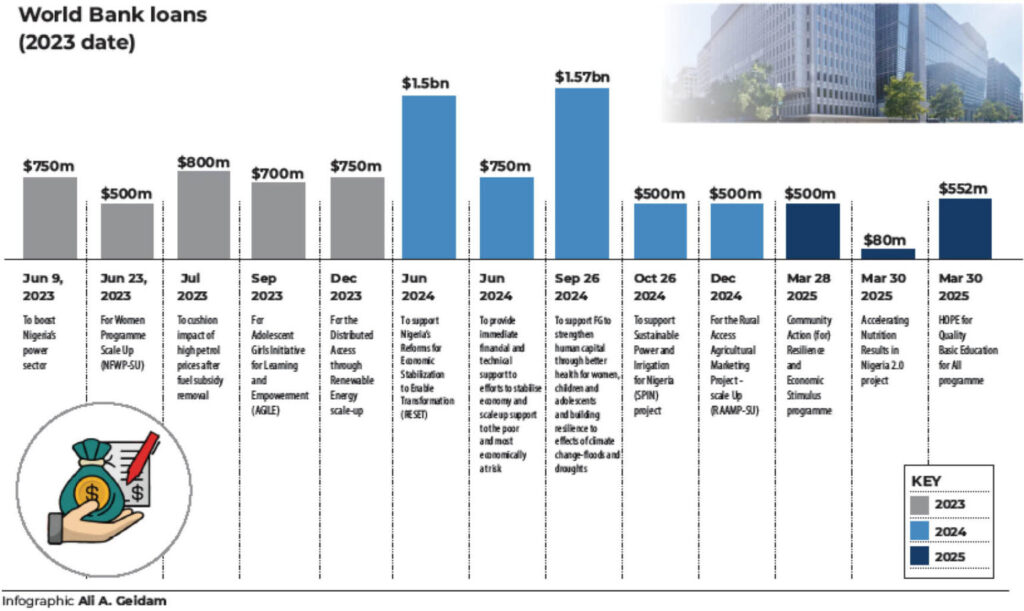

The World Bank has approved over ₦13.21 trillion ($8 billion) in loans for various developmental projects under Bola Tinubu’s administration in the last 20 months.

An analysis of these loans shows that they were allocated to multiple sectors of the economy, with three new loans totaling $1.1 billion approved between Friday and Tuesday.

According to data published by the Debt Management Office (DMO), Nigeria’s debt profile has now reached ₦142 trillion.

The 2025 Budget of N54.99 trillion has a debt service component of N14.32 trillion and N13.64 trillion for recurrent expenditure.

This development comes as the Central Bank of Nigeria (CBN) on Tuesday reported the highest Net Foreign Exchange Reserve (NFER) position as of the end of 2024.

According to CBN data released on Tuesday, the NFER stood at $23.11 billion, the highest level in over three years, Daily Trust reports.

This marks a significant increase from $3.99 billion at the end of 2023, $8.19 billion in 2022, and $14.59 billion in 2021.

The federal government is set to receive an additional $2.2 billion in loans from the World Bank in 2025.

Just last Friday, the World Bank approved a $500 million loan to support Nigeria’s Community Action for Resilience and Economic Stimulus Programme.

The loan, granted on March 28, 2025, is to provide essential support to households affected by economic downturns and strengthen community resilience.

Additionally, on Monday, the World Bank approved two more loans:

$80 million for the Accelerating Nutrition Results in Nigeria 2.0 project.

$552 million for the HOPE for Quality Basic Education for All programme.

With the latest approvals, Nigeria has secured $8.6 billion in loans from the World Bank in the past 20 months—excluding the $800 million support received in July 2023. This amounts to approximately ₦13.2 trillion at the current exchange rate.

The Lagos Chamber of Commerce and Industry (LCCI) has expressed concerns over the rising debt with the fresh loan from the World Bank.

While it acknowledged the loan’s direct impact on small businesses and vulnerable populations, through grants and livelihood support, it described the intervention as “a potential short-term stimulus.”

Director General of LCCI, Dr. Chinyere Almona, noted that Nigeria’s rising debt burden “is a growing concern, particularly given the slow pace of disbursement and implementation of previously approved loans.”

The chamber stated that with the World Bank’s share of Nigeria’s external debt reaching $17.32 billion, “the question of debt sustainability becomes increasingly pressing.”

Almona added that if the situation is not efficiently managed, “additional borrowing could exacerbate fiscal vulnerabilities, weaken investor confidence, and limit the government’s ability to execute long-term economic reforms.”

She stated that from a business perspective, while targeted stimulus programmes can offer temporary relief, structural economic challenges such as inadequate infrastructure, multiple taxation, and forex volatility remain unaddressed.

“Businesses require a stable operating environment, and while social welfare programmes are essential, they must be complemented by policies that foster productivity, investment, and job creation.

“There is also concern about the efficiency of funds allocation and utilisation, given that only 16% of previously approved World Bank loans under the current administration have been disbursed. This raises questions about the absorptive capacity of relevant institutions and the risk of funds being underutilised or mismanaged”, she said.

To fully maximize the benefits of these loans while reducing associated risks, the Lagos Chamber of Commerce and Industry (LCCI) emphasized the need for a transparent and efficient disbursement system to ensure that funds reach the intended beneficiaries, particularly small businesses and vulnerable communities.

The LCCI also urged the government to adopt a prudent debt management strategy that prioritizes concessional financing and ensures that borrowed funds are directed toward projects with clear economic returns.

“The LCCI maintains that a more effective stimulus for economic growth lies in addressing Nigeria’s persistent power supply issues and high energy costs while creating an enabling business environment where small businesses can thrive, generate jobs, and boost government revenues.”